Economy.

From interest rates to inflation, understand the impact of macroeconomic trends on the real estate capital markets…

The Beyond Insights series aims to deliver timely economic and market-driven insights to better inform your commercial real estate investment decisions.

Markets

From local market rents to cap rates, catch up on the latest capital markets insights.

Learn moreU.S. Economics: Macro Commentary & Insight

FNMA DUS Spreads Rip in November!

- A shift in market sentiment between FOMC meetings

- Projections of low future supply provide tailwind for spreads

Agency commercial mortgage-backed securities (CMBS) spreads rallied significantly over the month of November due to a positive pickup in investor sentiment. Cooling inflation coupled with a slightly weaker labor market has investors building confidence that the Fed has reached the end of their hiking cycle—volatility in the overall market has decreased over the course of the month. Spreads have caught a further tailwind from projections of the supply on bonds in the market remaining on the low end. Broker-dealers are accumulating balance-sheet positions while also filling strong end-account orders. Positive investor sentiment is projected to remain through year-end, barring any major macro shift.

The November rally in MBS spreads and U.S. Treasury rates highlights a shift in investor sentiment that occurred between the September and November Federal Open Market Committee (FOMC) decisions. The September FOMC meeting was somewhat of a shock to the market. The market fully expected that the Fed would pause the hiking campaign but did not expect the Fed’s projections for future rates moving forward. The FOMC released their updated Summary of Economic Projections and updated Dot Plot at the September meeting, which showed that 12 of 19 Fed officials see one more hike as necessary in 2023, while seven officials see a hold. Berkadia’s full coverage of the September FOMC meeting can be found here. The notion that the Fed would be holding rates “higher for longer,” coupled with the Dot Plot hinting that the Fed may hike rates again, drove uncertainty in the overall market. Treasury rates sold off, with the 10-year U.S. Treasury (UST) rate peaking at 5%. Agency MBS spreads widened following the FOMC meeting through the month of October after failing to recoup the typical widening at quarter-end.

Spreads continued to widen until the November 1 FOMC meeting: The FOMC held rates at the 5.25%–5.50% level and noted in the statement that tighter financial and credit conditions for households and businesses continue to weigh on the economy. The addition of “financial conditions” to the Fed’s statement was a surprise; previously the statement had only highlighted “credit conditions.” “Credit” might refer to banks making it harder to get loans, while “financial” suggests more of a market situation: Bloomberg Economics estimates that a persistent increase in long-term yields would substitute for 25–50 basis points of hikes, but failure for them to be persistent would necessitate another hike or two. Berkadia’s full coverage of the November FOMC meeting can be found here.

The addition of “financial conditions” reversed the market’s negative sentiment on the Fed’s Dot Plot. The market is no longer pricing in any additional rate hikes and is now awaiting cuts. MBS spreads were positively impacted by a fall in bond-market volatility, portrayed by the Merrill Lynch Option Volatility Estimate (MOVE) index in the chart below. Investment-grade credit default swaps, which tend to trade in tandem with Agency CMBS spreads, also tightened significantly over the month of November. The market seems to be reading the tea leaves and calling current levels the Fed’s terminal rate of this hiking cycle, while macroeconomic conditions continue to provide positive general sentiment for the market in the short term.

Agency CMBS spreads are being positively impacted by macroeconomic conditions as well as micro market projections. As noted in Berkadia’s previous spread commentary, found here, Agency CMBS spreads are highly affected by supply and demand. Market demand for bonds was restored in the month of November due to the positive sentiment shift, but the supply of bonds did not follow suit. Fannie Mae Delegated Underwriting and Services (FNMA DUS) production in October and November was over 50% lower in 2023 than it was in 2022. Current market sentiment is that supply will remain on the lower end in the short term, with strong demand and low supply continuing to provide positive momentum for spreads.

2023 2nd Half GSE Rate and Spread Movement

Dropping Bond Volatility & Tightening Credit Spreads

This commentary and any statements, information, data and content contained therein, and any materials, information, images, links, sounds, graphics or video provided in conjunction with this document (collectively “Materials”) has been prepared for informational purposes or general guidance on matters of interest only, and does not constitute professional advice, advertising or a solicitation. The Materials are of a general nature and not intended to address the circumstances of any particular individual or entity. You should not act upon the information contained in the Materials without obtaining specific professional advice. As such, nothing herein constitutes legal, financial, business, investment or tax advice and you should consult your own legal, financial, tax, investment or other professional advisor(s) before engaging in any activity in connection herewith. The information in the Materials is not a substitute for a thorough due diligence investigation. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in the Materials, and, to the extent permitted by law, Berkadia Commercial Mortgage LLC ( together with its affiliates, the “Company”) neither accept nor assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the Materials or for any decision based on them. No part of the Materials is to be copied, reproduced, distributed or disseminated in any way without the prior written consent of the Company.

Questions? Contact Us.

TIGHTER CREDIT STANDARDS AND BANK LIQUIDITY

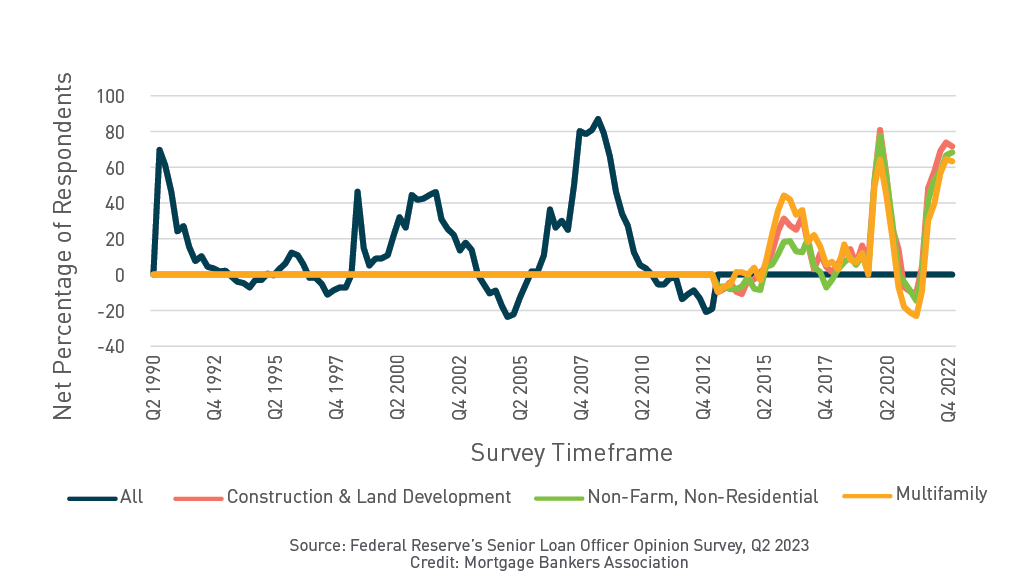

Commercial real estate lending by banks represents one of the largest blocks of available debt financing in the U.S. market. In the wake of the regional banking crisis, where three of the four largest American bank failures happened in the span of a couple months and the Federal Deposit Insurance Corporation was forced to take over, the attention of the market and regulators shifted to analyzing CRE lending and any complicity this sector had in the collapse of regional banks.

NET PERCENTAGE OF DOMESTIC RESPONDENTS TIGHTENING STANDARDS FOR COMMERCIAL REAL ESTATE LOANS

Be Berkadia Spotlight: Rene Coronado!

In today’s Be Berkadia spotlight, we feature Rene Coronado. Rene is the Asisstant Vice President for FHA Construction at Berkadia.

FHFA’s 2024 Multifamily Loan Purchase Caps Continue to Focus on Mission-Driven Housing

FHFA announced the 2024 multifamily loan purchase caps for Fannie Mae and Freddie Mac, here’s what’s required.

Insights From BOMA International’s 2023 MOB and Healthcare Real Estate Conference

Sabrina Solomiany, Berkadia National Head of Medical & Life Sciences, debriefs the recent BOMA International’s 2023 Medical Office Buildings and Healthcare Real Estate Conference.

Research and Insights

TIGHTER CREDIT STANDARDS AND BANK LIQUIDITY

Commercial real estate lending by banks represents one of the largest blocks of available debt financing in the U.S. market. In the wake of the regional banking crisis, where three of the four largest American bank failures happened in the span of a couple months and the Federal Deposit Insurance Corporation was forced to take over, the attention of the market and regulators shifted to analyzing CRE lending and any complicity this sector had in the collapse of regional banks.

NAVIGATING INSURANCE CHALLENGES IN CRE UNDERWRITING

Watch Berkadia’s Beyond Insights Webinar: Navigating Insurance Challenges in Commercial Real Estate (CRE) Underwriting, hosted on August 10, 2023. Danielle Lombardo, Chair, Lockton’s Global Real Estate Practice, provided her perspective into the significant tightening of the commercial real estate insurance market and the impact it’s had on premiums and coverage for multifamily investors.

Berkadia Study Argues CRE Lending Hasn’t Dried Up for Multifamily

“My initial hypothesis was we’d see a supreme dry-up in bank lending, and that just didn’t materialize.” said losh Bodin, senior vice president of securities trading at Berkadia, and one of the authors of the report. “While we’re seeing caution in bank lending, the second quarter supported the idea that there wasn’t nearly as much pullback as we thought there’d be.”